1952 continued the strong employment situation started in 1951:

The unemployment rate -- which was already low -- continued at it's strong rate, fluctuating between 3.4% and 2.7% for the year.

Total employees on all payrolls was more or less constant for the first seven months of the year, but really started to take-off in the last five months.

Goods producing industries were pretty constant for the the first five months of the year. They dropped over the summer, but then really took off. adding over 600,000 jobs in the last five months of the year.

Service producing industries saw better overall performance; they increased a bit during the first few months, leveled off, and then increased strongly in the last five months of the year. Overall, we see services adding a little under 1 million jobs for the year.

Growth in government employment mirrors the service industry chart for the year.

Thanks to a low rate of unemployment, we see strong growth in DPI:

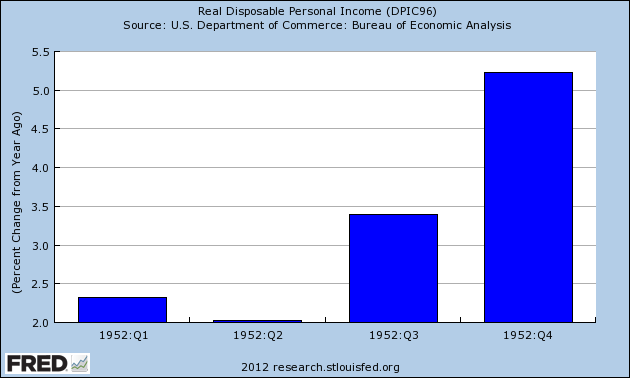

Total DPI increased every quarter in absolute (inflation-adjusted) terms.

The continuously compounded annual rate of change was weak in the first quarter, but picked-up momentum in the second and third quarter, and ended the year on a strong note.

The rate of change year over year was small in the first half of the year, but accelerated in the second.

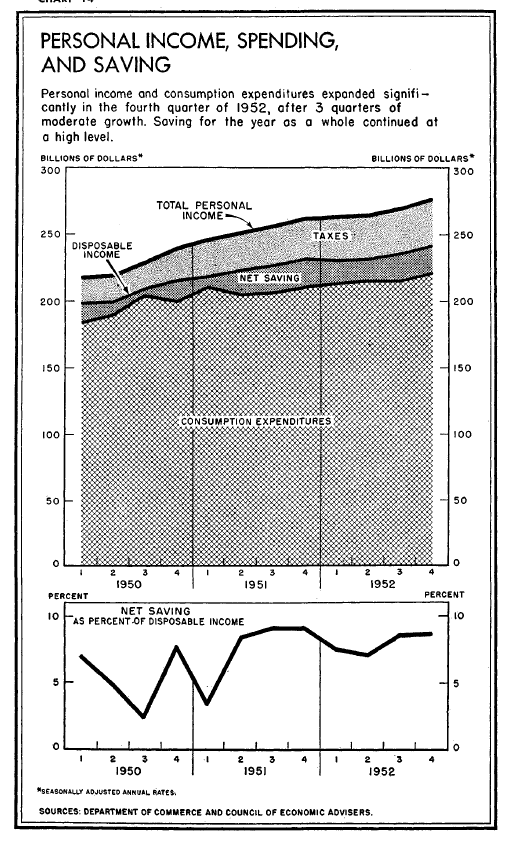

Finally, above is a chart from the 1953 Economic Report to the President that shows income and savings -- which was at a very strong rate in 1952.

The unemployment rate -- which was already low -- continued at it's strong rate, fluctuating between 3.4% and 2.7% for the year.

Total employees on all payrolls was more or less constant for the first seven months of the year, but really started to take-off in the last five months.

Goods producing industries were pretty constant for the the first five months of the year. They dropped over the summer, but then really took off. adding over 600,000 jobs in the last five months of the year.

Service producing industries saw better overall performance; they increased a bit during the first few months, leveled off, and then increased strongly in the last five months of the year. Overall, we see services adding a little under 1 million jobs for the year.

Growth in government employment mirrors the service industry chart for the year.

Thanks to a low rate of unemployment, we see strong growth in DPI:

Total DPI increased every quarter in absolute (inflation-adjusted) terms.

The continuously compounded annual rate of change was weak in the first quarter, but picked-up momentum in the second and third quarter, and ended the year on a strong note.

The rate of change year over year was small in the first half of the year, but accelerated in the second.

Finally, above is a chart from the 1953 Economic Report to the President that shows income and savings -- which was at a very strong rate in 1952.

{kind=link}