This was written by Invictus as well.There's widespread consensus that things are "less bad" of late than they were in the fourth quarter of 2008 or the first quarter of 2009. It's hard to disagree with that. However, when is the recession going to end, and what is going to become of the so-called "green shoots" that have taken the stock market from 666 in mid-March to almost 950 (on the S&P) recently?

Bonddad and I recently

did some work advancing the notion that the consumer -- who has been 70 percent of GDP for the past eight years -- is over-levered and in no shape to continue shouldering that burden for the foreseeable future. It's my belief that the recovery, when it comes, is going to be shallow at best, and it's not out of the question that we double-dip (assuming we actually emerge) after miniscule positive growth triggered by replenishment of the massive inventory draw-downs we've seen in the past couple of quarters.

But let's not get ahead of ourselves. When will the recession end? We know that the

National Bureau of Economic Research (NBER) will not date the end for quite some time to come.

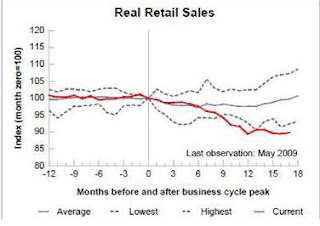

Aside from GDP, we know that the NBER looks at many other measures of our economy's health. Most notably (in what I believe may be their order of importance) are Employment (PAYEMS at St. Louis Fed), Industrial Production (INDPRO at St. Louis Fed), Real Income, and Real Retail Sales.

Here's a look at how those four metrics look of late relative to other recessions (via St. Louis Fed):

We also know -- because he's told us -- that one member of the NBER's Business Cycle Dating Committee, professor Jeffrey Frankel, likes to look at the Aggregate Weekly Hours Index (AWHI), since employers typically cut hours before they cut bodies, and similarly increase hours before they hire bodies.

Here's what that looks like:

It is certainly difficult, if not impossible, to argue that anything has actually troughed as yet. And employment will undoubtedly not pick up until after hours are increased and employers feel that they actually need additional bodies.

Another area that the "green shoots" crowd points to is Unemployment Claims, a high-frequency (weekly) number that has shown signs of stabilization and, arguably, slight improvement.

Even continuing claims -- an important metric that needs to confirm the weekly number -- has recently (last week) improved (by a meaningful -148,000):

Now, don't get me wrong, I'll take what I can get. But pulling back the lens a bit, this is what the improvement looks like from a longer-term view:

Bottom line: While there may be some justification for cautious optimism, the key and operative word must remain "cautious." As to calling the end of the recession -- notwithstanding any positive GDP print we might get over the next quarter or two -- it doesn't seem we're quite there just yet. We will, of course, continue to monitor the available data for signs of a trough. While we will no doubt emerge from recession eventually, attention should be paid to the type of recovery we can muster, and how we're going to re-employ the six million Americans who've lost their jobs over the past eighteen months.